Uncorrelated Returns

Combining several independent return streams beats picking any single one. This builds the portfolio: cluster a multi-asset universe by correlation, then balance risk across the clusters.

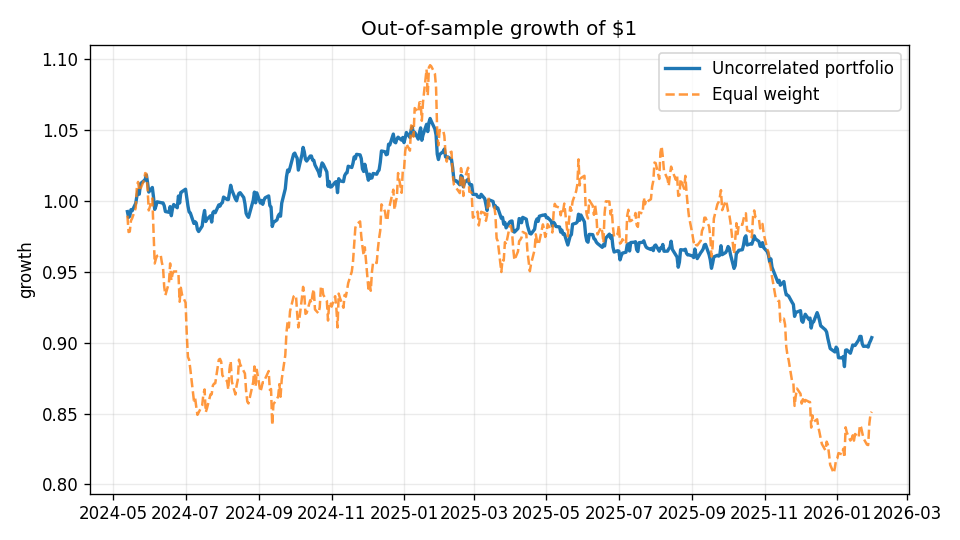

6.65%

portfolio vol (vs 15.3% equal-wt)

1.83

diversification ratio

−16.5%

max drawdown (vs −26.2%)

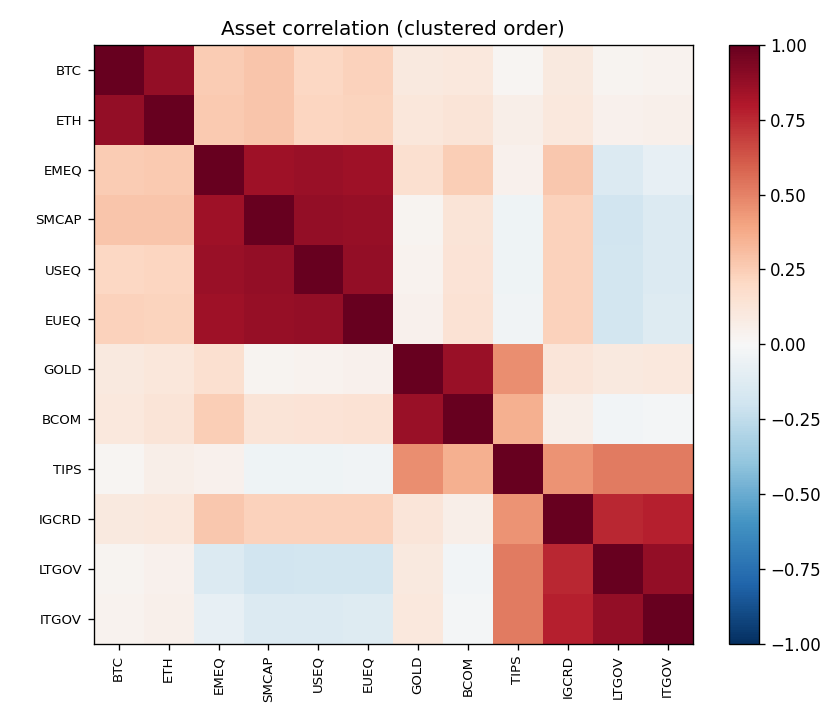

12 → 6

assets clustered into themes

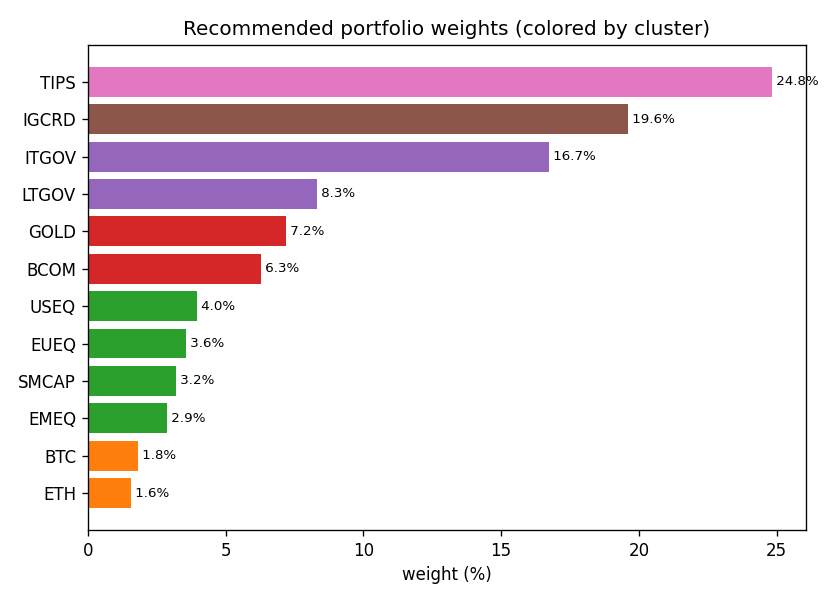

The recommended portfolio

Inverse-vol within each cluster, risk parity across clusters — so a calm bond sleeve and a wild crypto sleeve each contribute the same risk.

How it works

1 · Cluster

Correlation → distance √(½(1−ρ)) → hierarchical clustering, k chosen by silhouette.

2 · Weight within

Inverse-volatility weights inside each cluster.

3 · Balance across

Risk parity over the cluster streams (SLSQP), equalizing risk contributions.

4 · Evaluate

Train/test split; report vol, drawdown, Sharpe, diversification ratio.

Run it

pip install -e ".[dev]"

uncorrelated --plots docs # clusters, weights, performance + charts

uncorrelated --source live # use real market data (yfinance)