Time-Series Momentum

An asset's own past direction predicts its next move. Volatility-scale that signal across many markets and you get a diversified, risk-targeted trend-following strategy — implemented and backtested here.

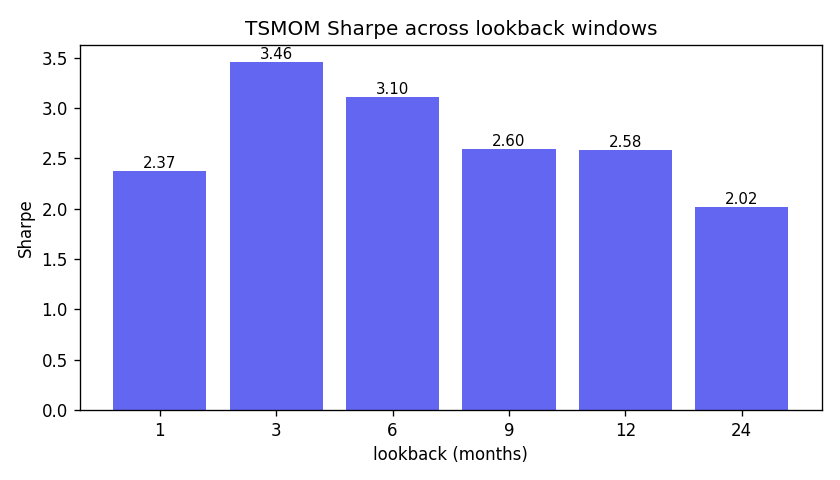

2.58

Sharpe (vs −0.27 long-only)

7.6

predictability t-stat

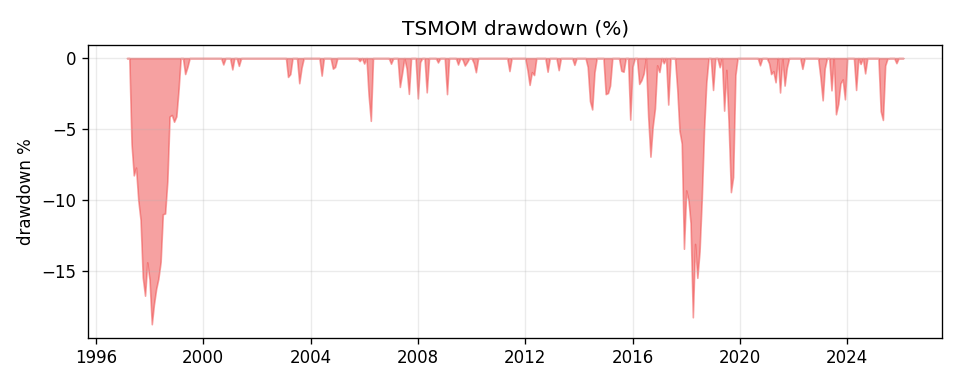

−18.7%

max drawdown (vs −83.7%)

75%

monthly hit rate

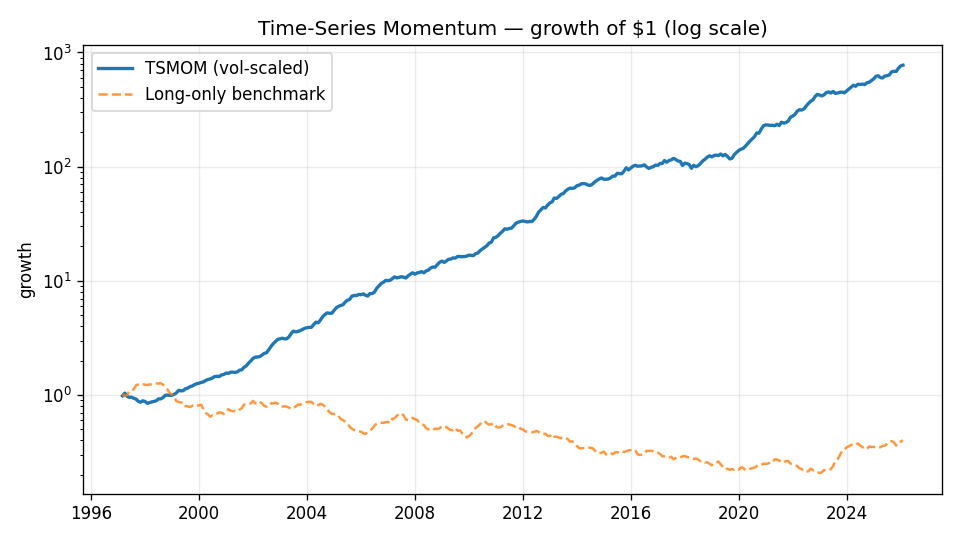

The backtest

Vol-scaled long/short positions, monthly rebalance, only past information used. Growth of $1 on a log scale:

The rule

signal = sign(trailing 12-month return) # +1 long / −1 short

position = signal × target_vol / ex_ante_vol # equal risk per asset

return = position × next-month return # average across assetsNumbers above use synthetic data built with persistent trends, to show

the mechanism cleanly. Real markets are noisier — run tsmom --source live

to backtest on actual prices via yfinance.